US Economic Outlook | January 14, 2026

Make-Up Work

As data gaps are closed, the economy’s resilience has been affirmed.

Taking time away due to illness is never ideal. Upon return to school or work, we are greeted with all the tasks we did not complete while incapacitated. The recovery may feel worse than the disease.

We are still recovering from the affliction of a record-setting federal government shutdown, which halted the publication of key economic statistics. We still haven’t fully recovered our sense of conditions, but nothing we have seen has altered our sense that the U.S. economy remains resilient.

A new year offers an opportunity to chart a new course. 2026 could bring some relief to U.S. households and businesses. Income tax refunds are poised to increase, trade deals may take shape, and housing affordability proposals are coming into focus. Policy uncertainty will feel less shocking, while the short-term interest rate outlook stabilizes. The low-turnover job market seems bound to break one way or the other: some sectors may see hiring, though layoffs could take hold in others.

Following are our thoughts on the U.S. economy.

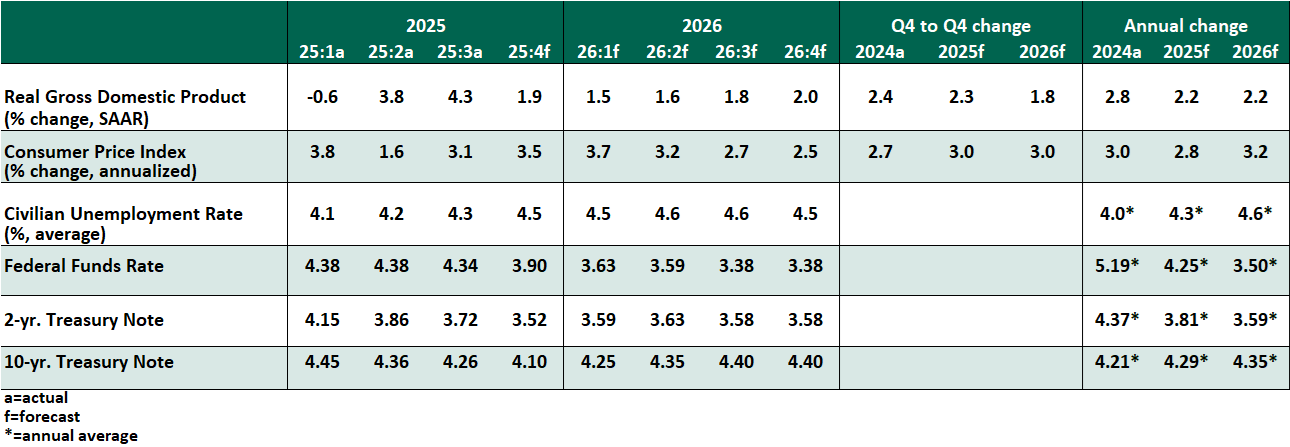

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

- Economic activity remained robust through the third quarter, with inflation-adjusted gross domestic product gaining 4.3% at an annualized rate. Consumer spending carried on its five-year winning streak, growing 3.5%; consumption may be uneven, but it is not slowing. The trade balance receded as imports continued to cool, supporting the strong headline. However, construction remains in a slump, with declines across both residential and business investment in structures.

- The labor market has settled into a slow, stable state. The combined October-November employment report showed a new cycle high for the unemployment rate and significant job losses due to the buyout-related departure of federal government workers at the end of September. The unemployment rate moderated to 4.4% in December. Excluding the disrupted government category, the private sector showed job gains of 1,000, 50,000, and 37,000 in October, November and December, respectively. The healthcare and hospitality sectors have led gains each month, with most others flat or slightly declining.

- Inflation has eased, measuring 2.6% year over year on a core basis (excluding food and energy) in both November and December, as compared to 3.0% in September. Price collection was suspended in October, leaving a gap for most categories. The untested methodology used to bridge missing October observations and late data collection in November may have understated actual changes, particularly for shelter.

Annual price adjustment cycles have led to larger increases in inflation in January of recent years. The strongest evidence of tariff-driven inflation is likely still in store.

Consumption data, including the Fed’s preferred inflation indicator, remains disrupted from the shutdown and will not return to its usual cadence until March.

- At its December meeting, the Federal Open Market Committee lowered the Fed Funds rate by 0.25% to a range of 3.50-3.75%. The accompanying statement and Summary of Economic Projections set clear expectations for a slower pace of easing ahead. We anticipate one cut in the first half of 2026 before a prolonged pause.

Dissenting votes in both directions show the difficulty of setting policy. Slower employment calls for easing, but firm inflation pushes against stimulating the economy with lower borrowing costs. The minutes of the meeting noted that some Committee members who supported the cut would have also been comfortable keeping the rate unchanged. Whoever rises to the role of Chair this year will inherit a committee with widely varied opinions.

The Fed’s approach to its balance sheet has pivoted quickly in response to evidence of lower liquidity in overnight funding markets. An end to quantitative tightening was announced October 29 and implemented December 1. As funding rates remained firm, the Fed responded by allowing reserve management purchases of up to $40 billion per month to ensure liquidity in short-term assets. While not a return to quantitative easing, the decision shows the Fed’s support for market function.

- Concern over hidden credit risks has not yet grown into anything systemic. Increases in volatility in October and November were short-lived, and brief market swoons may be the new norm. Overall financial conditions remain constructive to growth.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.