Weekly Economic Commentary | March 20, 2026

Central Banks Attempt To Peer Through The Fog

Price stability enters a new cycle of uncertainty.

By Carl Tannenbaum

On New Year’s Eve, 1988, the Chicago Bears and the Philadelphia Eagles met in an NFL playoff game. During the second quarter, a dense fog descended on the stadium. For the next two hours, players, officials and commentators struggled with very limited visibility. When the air finally cleared, the Bears had won what became known as “The Fog Bowl.”

Economic players, officials and commentators are presently struggling to see through what is known as “the fog of war.” Uncertainty surrounding the course of conflict in Iran and its impact on countries and commodities is high, making decision-making difficult. That was the backdrop for a long series of central bank meetings this week.

Coming into 2026, forecasters were expecting short-term interest rates around the world to decline modestly. Inflation remains above targeted levels in many countries, but it has been declining from its pandemic highs. Tariffs placed upward pressure on the prices of some goods, but haven’t yet had the inflationary impact that some have feared. Easier monetary policy was on the horizon.

And then, the war arrived, bringing with it a series of supply shocks. While energy is at the center, other commodities have also been affected. Each week that goes by without resolution increases dislocations.

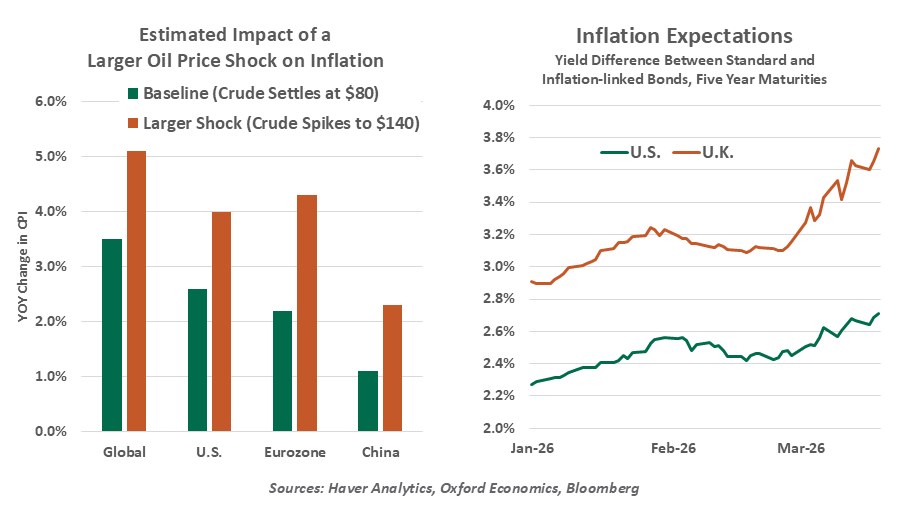

Energy prices are the most direct channel of transmission from the war to economic variables. But the costs of oil and gas influence the prices of a range of goods through the costs of transportation. Insufficient energy supplies could hinder output of a range of products, including microchips. Petroleum is an input to plastic resins, and byproducts of the refining process are used in agriculture and the processing of minerals.

We are experiencing supply chain disruptions that will take time to correct. Ships find themselves out of position, with downstream impacts to other points in the logistics system. This can add to prices and inflation.

Energy prices also influence expectations. Since the war began, measures of inflation expectations have risen: changes have been more pronounced for Europe than the U.S., and higher for shorter terms than longer ones. Because the psychology surrounding prices can allow inflation to become more deeply entrenched, central banks seek to keep expectations well-anchored.

As a guideline, economists estimate that every sustained $10 increase in the cost of a barrel of oil produces a 0.2% increase in consumer prices. The impact will tend to fade over time, as prices stabilize at a new level. For that reason, central banks tend to “look through” temporary energy shocks when assessing inflation and setting monetary policy.

The war will have a series of influences on inflation.

While they last, increases in inflation also tend to hinder economic growth. They act as a tax on households and businesses, reducing real incomes and spending. The impact on activity in the United States is expected to be modest; the economy is still being buoyed by the technology investment boom, and this year’s tax refunds will add to disposable income. But for other markets, economic impacts could be much greater.

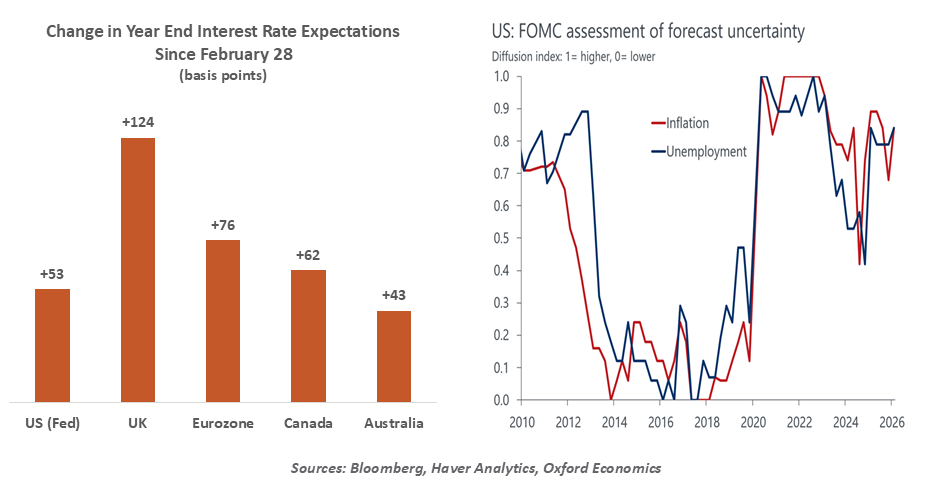

These opposing influences on inflation—direct upward pressure from commodities prices and indirect downward pressure from slower economic growth—are terribly difficult to balance. Markets have rushed to the conclusion that inflation risk would significantly alter trajectories for interest rates across regions; central banks had their first opportunities to weigh in this week.

The formal statement from the Federal Reserve expressed that the effects of the war remain uncertain, a theme which was repeated by Chairman Jerome Powell during his press conference. The consensus forecast released after the meeting reflected higher levels of both inflation and inflation risk, which informed the decision to hold rates steady. A majority of the Federal Open Market Committee still sees one rate cut this year, but our view is that it will come much later than previously thought.

The war provided the Bank of England a rare window of clarity. For the first time in over four years, the Monetary Policy Committee was unanimous in a decision; rates were held stable, but the group’s messaging warned that rate hikes could be on the horizon. British inflation took longer to settle down after the pandemic, and inflation expectations in the U.K. are elevated. Markets are now expecting that short-term rates in Britain will be much higher at the end of 2026.

The euro area is likely to experience a fairly significant economic shock, as the war has caused natural gas prices on the continent to more than double. The European Central Bank (ECB) reduced its expectations for growth, and raised its projections for inflation. While financial markets are expecting the ECB to raise interest rates later on this year, we think that prospect is less likely.

The changing interest rate outlook will be uncomfortable for borrowers.

Across markets, the war has taken interest rate cuts off the table, at least for a while. This will not be a welcome development for governments, who have been hoping that lower rates would ease the burden of servicing national debts. This will be particularly impactful in the U.K., where government bond yields have jumped and where budget tolerances are tight.

The turn of events will also create an additional complication for the succession at the top of the Federal Reserve. Legal issues surrounding the Chairman are delaying confirmation hearings for Kevin Warsh, and his challenge of mediating between the White House and the financial markets on policy has become even more difficult.

The skies over Chicago cleared within an hour after The Fog Bowl ended. Unfortunately, the fog of war that is clouding the global economic outlook is unlikely to lift anytime soon.

Related Articles

Meet Your Expert

Carl Tannenbaum

Chief Economist

Carl Tannenbaum is the Chief Economist for Northern Trust. In this role, he briefs clients and colleagues on the economy and business conditions, prepares the bank's official economic outlook and participates in forecast surveys. He is a member of Northern Trust's investment policy committee, its capital committee, and its asset/liability management committee.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.