Weekly Economic Commentary | February 6, 2026

Will Kevin Warsh Rebalance The Fed?

Reform proposals will face high hurdles.

By Carl Tannenbaum

At the start of my career, the Federal Reserve was content to operate in the shadows. Today, by contrast, the Fed is a much more public entity. And so the fact that the derby to become the next Chairman played out so vividly in the media was not surprising. The selection of Kevin Warsh ends one chapter of suspense, but opens others.

Warsh is hardly an unconventional choice. He spent five years on the Fed’s Board of Governors, serving as a critical liaison with Wall Street during the 2008 financial crisis. He was a staunch inflation hawk during that interval, and his statements since do not suggest any wavering in his commitment to price stability.

Despite being a known quantity, Warsh will have to engender confidence from a broad range of communities. The U.S. Senate will be first among them; confirmation hearings will be colored by the investigation of current Fed Chair Jerome Powell. Legislators, not to mention the financial markets, will be anxious for a pledge of allegiance to Fed independence.

If and when he is seated, Warsh will have to find common ground with leaders and staff at the Board of Governors. He has criticized Fed “groupthink” and overreliance on models developed by what he has derisively referred to as “the economics guild.” Last July, he observed that “What we need is regime change at the Fed, and that’s not just about the chairman, it’s about a range of people…It’s about breaking some heads.”

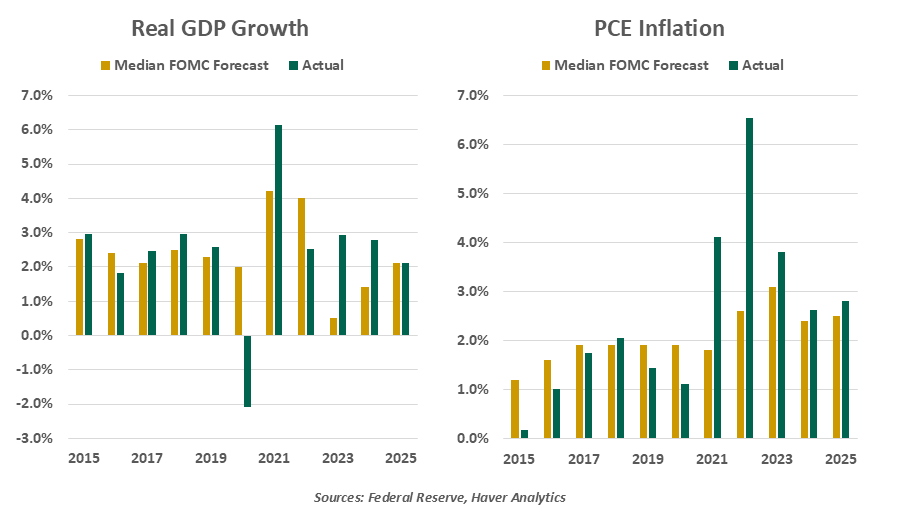

The Fed’s recent forecasting record is not something to be proud of. (In that, they have lots of company.) But the utility of macroeconomic models is not confined to point accuracy. They provide some structure to think about economic dynamics; because monetary policy works with a lag, central banks need tools that will help them anticipate how inflation will evolve. Models can always use improvement, but doing away with them is not an option.

Forecasting is especially complicated in the current day. Data interruptions related to last fall’s U.S. government shutdown have not fully been repaired. Tariffs are still working their way through to inflation, and debate is active over whether they will have a transitory or more lasting impact. To top it all off, some are suggesting that we are on the verge of another Great Moderation in which strong productivity gains may allow for lower interest rates without raising inflation risk.

Warsh aims to tackle the “economics guild.”

Many members of the economics guild may soon be Kevin Warsh’s colleagues, and he’ll need to find common ground with them. At least initially, Warsh will be outnumbered by senior Fed officials who have less discomfort with the status quo.

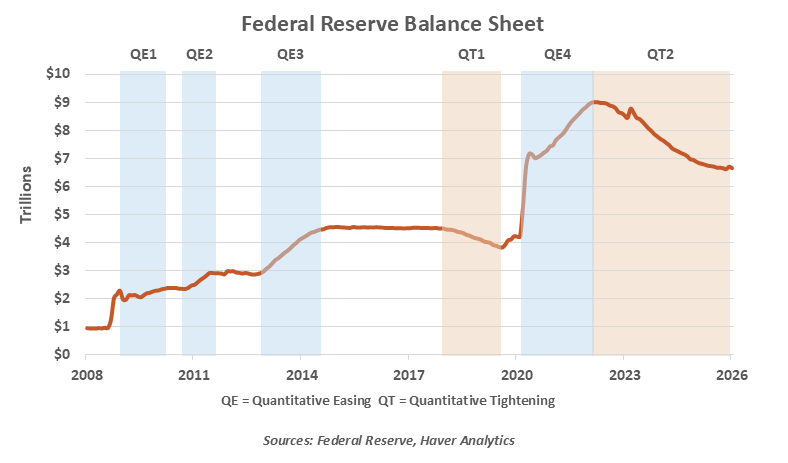

Warsh has also been a consistent critic of the Fed’s use of its balance sheet. As a Fed governor, he became increasingly uncomfortable with quantitative easing (QE), the Fed’s practice of purchasing securities to add liquidity to the financial system. Meeting transcripts from Federal Open Market Committee meetings in 2010 show that Warsh voted against extending QE, saying that it had “gone past the point of diminishing returns.” The Wall Street Journal reported last week that Warsh left the Fed in frustration over this strategy.

In a recent editorial, Warsh criticized the Fed’s “bloated balance sheet,” and suggested that it could be reduced substantially. Warsh’s chief concern is that the Fed’s accumulation of Treasury securities has facilitated fiscal recklessness and distorted asset allocation in the private sector. The Fed currently holds about 13% of government debt outstanding; this is a lower proportion than other central banks, but significant nonetheless.

To this observer, there is little doubt that the Fed’s use of QE helped to prevent the stress of 2008 and 2020 from turning into a lasting malaise. Studies of QE’s effectiveness outside of those intervals have not found conclusive benefits. And optically, it appears as if the Fed has been enabling excessive fiscal expansion. Warsh finds fault with the Fed on both of these grounds, and has gone further to suggest that the Fed’s efforts to contain unemployment have led it into policy areas that would be better handled by Congress.

There are two problems with reducing the Fed’s balance sheet, one technical and one political. When the Fed sets a target for overnight rates, this outcome does not happen by fiat. The Fed’s open market desk has to steer toward that outcome by transacting in government securities. When liquidity in the bond market is limited, the Fed struggles to hit the mark. As we discussed in an article late last year, the Fed must maintain a fairly sizeable collection of government bonds simply to execute basic monetary policy.

It will not be easy to reduce the Fed’s balance sheet.

The political aspect is that limiting the Fed’s holdings has the potential to raise long-term interest rates: removal of an important buyer will keep bond prices lower and yields higher. This runs counter to the administration’s desire to keep borrowing costs low. Because Treasury rates drive mortgage rates, this would exacerbate the affordability problems that have taken center stage in recent months. Fiscal deficits are deep, and extend as far as the eye can see. If the Fed steps back, someone else is going to have to buy a lot of Treasury debt.

The White House expressed the hope that Kevin Warsh “will go down as one of the great Fed chairmen.” But those warm feelings could dissipate quickly, as they did when Jerome Powell was selected in 2018. Keeping all stakeholders happy will be a tall order.

When I worked at the Fed, I participated in system conferences at which Kevin Warsh was a featured speaker. I was impressed with his communication skills and his insights on leadership. He’ll need to apply both in large measure in the months ahead.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.