Weekly Economic Commentary | April 24, 2026

The Gulf May Need New Vision

Bold strategic plans have met real-world obstacles.

By Carl Tannenbaum

Leaders often have trouble focusing on the longer-term. In the corporate arena, pressure to produce quarterly earnings can truncate planning horizons. In public life, popular opinion and election cycles can impose myopia. It takes a unique set of ingredients to set, and stick to, a lasting vision.

The six nations (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates) that compose the Gulf Cooperation Council (GCC) have those ingredients in place. Their immense wealth and their dynastic leadership provided a foundation to think far into the future, and the ability to deliver on their ambitions. Several Gulf countries issued long-term plans for what they hoped to achieve by the year 2030.

2030 isn’t that far off any more. But some of the goals within the Gulf’s long-term vision statements seem a long way off. Nations were scaling back their ambitions before the war with Iran began, and will likely have to reconsider them further in the wake of the conflict. This will have important implications for Gulf countries, and for the rest of the world.

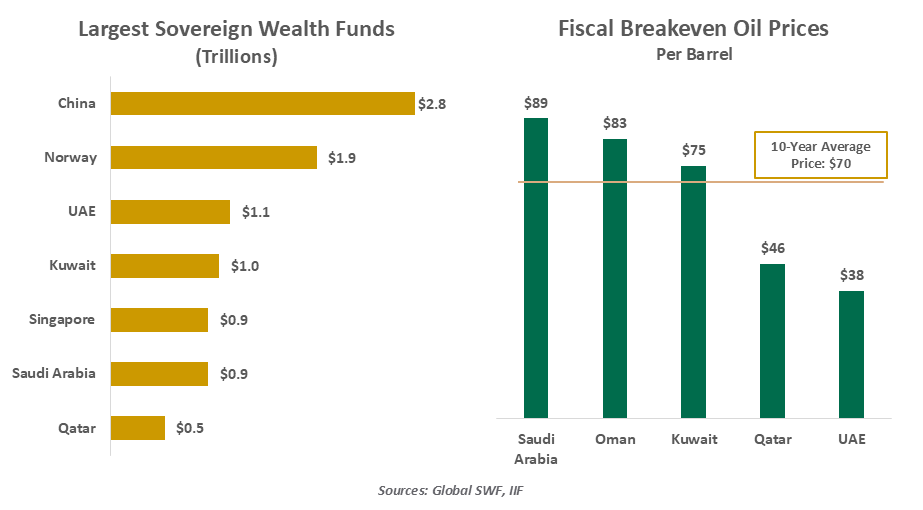

The GCC has a small population (just 60 million people), but it casts a big footprint on the global economy. Its oil is a substantial source of revenue and influence, and its wealth has facilitated substantial domestic and international investments.

Gulf countries are aware that the “blessings” of petroleum reserves are not infinite. The benefits that they offer to their citizens are reliant on relatively high prices for oil (known as “fiscal breakevens”). To transition to more sustainable models, several Middle Eastern nations drafted outlines for long-term economic change. Saudi Arabia’s edition, known as Vision 2030, was the most prominent. The strategies sought economic diversity through the promotion of non-oil industries.

Increased tourism was a common objective. Saudi Arabia set out to build a massive cultural and entertainment hub in Qiddiya City. The United Arab Emirates (UAE) created Yas Island in Abu Dhabi, complete with a Formula One race track. Member states also sought to enhance their profiles as centers of technology and innovation; Saudi Arabia launched NEOM, a technology-focused planned city intended to house 1.5 million residents.

Gulf countries were revisiting their economic plans long before the war started.

Financial services were also targeted for additional emphasis. Capital inflows to GCC countries have increased, amid significant investment in financial technology. The capitalization of GCC stock exchanges is in excess of $4 trillion.

To finance these endeavors, GCC countries utilize sovereign wealth funds, which are endowed with trillions of dollars. On top of that, Gulf states set out to attract billions of foreign investment each year. The UAE has shown the most significant progress, driving the price of oil needed for fiscal balance down below $40.

Ironically, the desires of GCC countries to diversify away from oil were contingent on the continuation of oil revenues. While global petroleum demand has continued to increase over the past decade, increased supplies from the United States have more than compensated. Crude prices have not met the levels assumed when grand plans for 2030 were formulated.

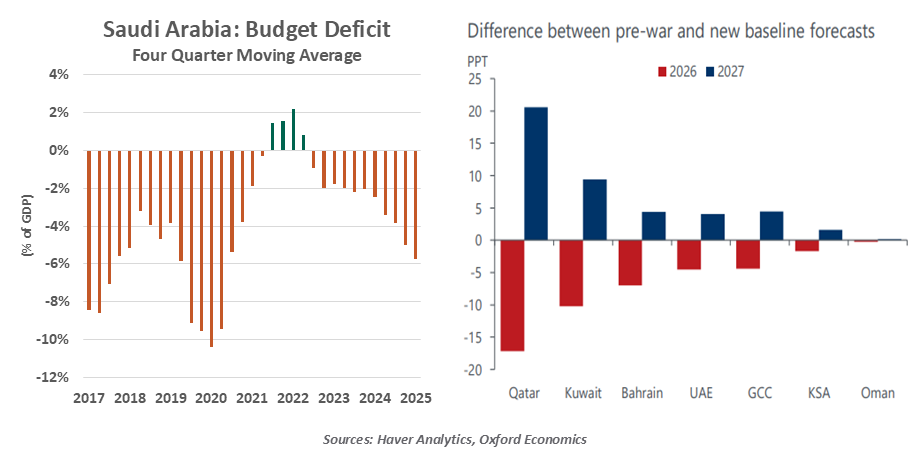

Saudi Arabia has been most impacted. After a brief surplus in 2022, the national budget deficit has been expanding in recent years. In response, the scale and scope of Vision 2030 programs were re-evaluated. The Saudi Public Investment Fund (PIF) reduced spending on portfolio projects by 20% last year, with some initiatives cut by much more than that. Despite these measures, rating agencies expressed concern over Saudi’s fiscal position this past March.

And then the war arrived. The fighting in the region has had a significant impact on members of the GCC. With shipping of petroleum severely constrained, production and revenue have been reduced. Some countries have sustained damage from Iran’s attacks, and will need to deploy resources for repairs. Environmental impacts will need to be addressed. Recessions are forecast for several states.

Rebounds are anticipated once the war ends, but there may be long-term damage done to regional economies. Security concerns will almost certainly cause providers of capital to the GCC to rethink their allocations. The willingness of travelers to venture to the region may be diminished; the region is projected to lose between $35 billion and $60 billion in tourism revenue during the balance of this year alone.

Changes in investment flows from the Middle East would have global implications.

As we discussed last month, the war will almost certainly lead countries to renew their thinking about energy security. Sourcing hydrocarbons from different places, accelerating the green transition, and additional use of nuclear power are all under consideration. As these strategies are put into place, the value of Middle Eastern oil may fall.

It could become more difficult for GCC countries to sustain inbound investment, given heightened risks. Sovereign funds in the region have stated that they will follow through on existing overseas commitments, but they may need to turn inward going forward. Prospective recipients of their outbound investment may need to look elsewhere; their costs of capital will increase. It also bears noting that GCC nations own about 3.5% of outstanding Treasury securities.

We tend to judge plans solely by the results they produce. That may be a little harsh: strategies are established using information available at the time, which is subject to change. As Gulf countries refresh their visions, they’ll have to account for new regional realities.

Related Articles

Meet Your Expert

Carl Tannenbaum

Chief Economist

Carl Tannenbaum is the Chief Economist for Northern Trust. In this role, he briefs clients and colleagues on the economy and business conditions, prepares the bank's official economic outlook and participates in forecast surveys. He is a member of Northern Trust's investment policy committee, its capital committee, and its asset/liability management committee.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.