Weekly Economic Commentary | February 13, 2026

U.S. Housing Market: A Fixer-Upper

Ideas for housing reform are developing rapidly.

By Ryan Boyle

Browsing real-estate listings is a popular hobby. Home data portals provide hours of free entertainment. Some listings feature bizarre or ostentatious decoration; some are time capsules, preserving a bygone era. Most entries share one shocking feature: the price.

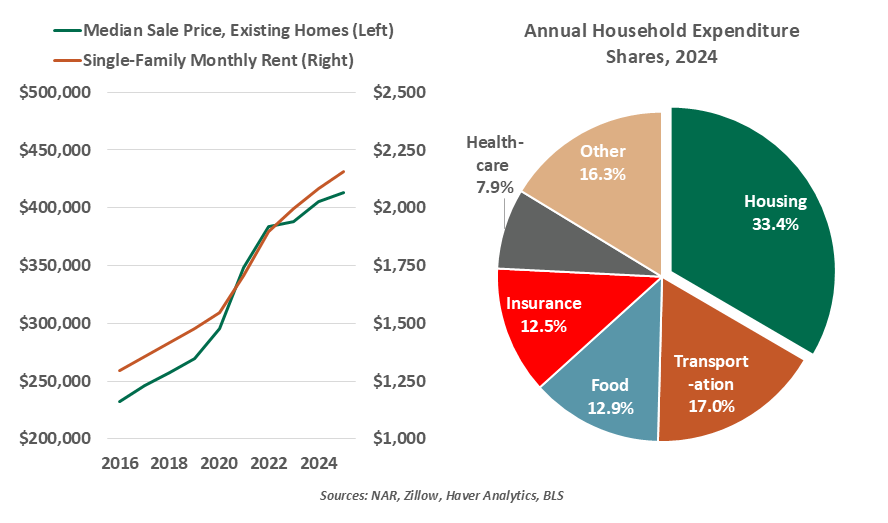

Whether renting or owning, city or suburbs, condo or castle: U.S. housing is expensive. In aggregate, U.S. households spend a third of their budgets on shelter. This large monthly expense adds to the ongoing perception of strained affordability.

The ads showing outdated homes illustrate the broader phenomenon of more seniors choosing to age in place. Their homes are comfortable and familiar, while downsizing and moving are difficult and disruptive. They are holding on to their homes as long as they can. And a younger cohort of current homeowners are also feeling stuck, as upgrading would entail a higher purchase price financed at a substantially higher interest rate.

Fewer transactions lead to tighter supply, which keeps house prices elevated and further out of reach. Can policy measures break this cycle of decreasing affordability?

To our economists’ eyes, the solution seems simple. When demand exceeds supply, add more supply! But we have chronicled the structural challenges to building. Construction costs are high, labor is sometimes scarce, and local zoning can be an obstacle. Even a full-tilt effort to build housing, akin to the recovery following World War II, would take years to meaningfully increase inventories.

With affordability remaining in focus, the administration is seeking ways to reduce the cost of housing. Interventions must strike a balance of making housing more affordable, while neither sparking inflation nor causing existing homeowners to lose wealth. Many ideas are in discussion, with some becoming tangible.

Ideas for housing market reform are abundant, but change will take time.

Congress is working to reform housing. This week, the House passed the Housing for the 21st Century Act. The bill moves to standardize local zoning and land use laws, simplifies construction environmental reviews and removes regulations that had impaired manufactured housing. The Senate is working toward similar reforms. These changes are minor, and results will be slow, but they all move in the direction of adding to housing supply.

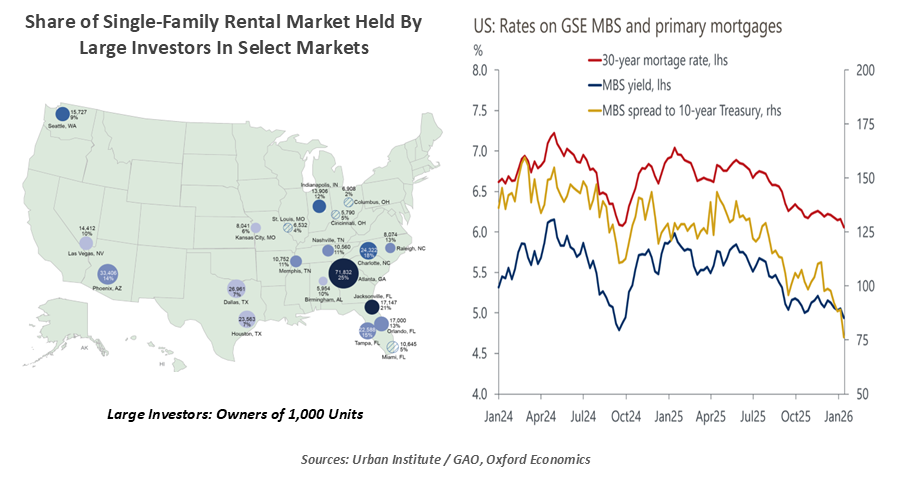

President Trump has directed Fannie Mae and Freddie Mac (which are government-sponsored entities, or GSEs) to deploy $200 billion of liquid assets to acquire more mortgage-backed securities (MBS). The GSEs acted quickly, and mortgage spreads fell by about 10 basis points in January; they are unlikely to fall further. This order suggests the president is content to keep the GSEs under federal control; that cash was being accumulated to move toward the long-rumored GSE privatization. A return to private ownership would likely raise mortgage rates, so we are not surprised to see that idea fall to the wayside.

Reform proposals might buy time while construction catches up.

The president has also pushed to prevent large institutional buyers from purchasing any single-family housing. These buyers represent less than 3% of national ownership, albeit with higher concentrations in select regions. Unless they were forced to liquidate their holdings, they are unlikely to alter the supply of housing. A drawback to this approach is that such a regulation would impair future investment. Large-scale owners emerged as a wave of foreclosed homes came to market in the early 2010s, keeping the housing stock available as rentals. Removing a buyer of last resort could compound future stress in the market. An Act of Congress would be required for this policy, and it seems unlikely to be taken up.

Policymakers and advocates have floated other ideas:

- 50-year mortgages: Longer terms would mean lower monthly payments, but at a cost of 20 additional years of interest on a loan. 30-year terms are already the longest in the world; a 50 year term would act more as a long-term rental arrangement.

- Allow 401(k) retirement savings to be used for housing: While more buyers would be able to make a down payment, it would set back their retirement progress and reset the benefit of compounding returns. Most savers can borrow from their retirement accounts already.

- More rent-to-own development: Builders have proposed a plan for tracts of affordable “Trump Homes,” in which long-term occupants could become homeowners. Even without a purchase option, build-to-rent housing can help add to supply. However, affordable homes offer lower margins to builders and are more likely to encounter local ordinance complications.

- Exemptions to building material tariffs: Most tariff policies have carved out strategic sectors, and a case can be made to extend these to the lumber and metals used in housing.

- Antitrust investigations of home builders: Market power will be difficult to prove. Even a successful legal case will be slow and unlikely to change the housing market.

- Portable or assumable mortgages: Allowing borrowers to carry their loans to another property, or sell their mortgage to a buyer along with the property, would disrupt the mortgage industry and alter credit underwriting.

- Fed asset purchases: While asset acquisitions could help to hold down MBS or benchmark Treasury yields, the Chair-to-be would prefer a smaller balance sheet.

Each of the above ideas have high hurdles to implementation, and we discount them all as unlikely to happen. The breadth of suggestions shows that reforms may evolve and adapt. Most of them are stopgap measures that would offer limited relief while the slowest but most important change is made: more building.

Reconstructing the housing market will be a long-running exercise. I’ll use my real estate apps to gauge progress. One day, we may stop marveling at prices, and instead remark at the volume and variety of new construction.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.