'%3e%3cpath%20d='M14.5584%2010.5857L23.6652%200H21.5072L13.5999%209.19156L7.2843%200H0L9.55034%2013.8992L0%2025H2.1582L10.5087%2015.2935L17.1783%2025H24.4626L14.5582%2010.5857H14.5588H14.5584ZM11.6025%2014.0215L10.6348%2012.6375L2.9357%201.62451H6.25036L12.4638%2010.5123L13.4315%2011.8963L21.5082%2023.4491H18.1935L11.6027%2014.0219V14.0213L11.6025%2014.0215Z'%20fill='%23808182'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_20_84'%3e%3crect%20width='24.4624'%20height='25'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

%20is%20a%20leading%20provider%20of%20wealth%20management,%20asset%20servicing,%20asset%20management%20and%20banking%20to%20corporations,%20institutions,%20affluent%20families%20and%20individuals.%20Founded%20in%20Chicago%20in%201889,%20Northern%20Trust%20has%20offices%20in%20the%20United%20States%20in%2019%20states%20and%20Washington,%20D.C.,%20and%2020%20international%20locations%20in%20Canada,%20Europe,%20the%20Middle%20East%20and%20the%20Asia-Pacific%20region.%20%3c/desc%3e%3cpath%20fill='%233d4042'%20d='M21,21H17V14.25C17,13.19%2015.81,12.31%2014.75,12.31C13.69,12.31%2013,13.19%2013,14.25V21H9V9H13V11C13.66,9.93%2015.36,9.24%2016.5,9.24C19,9.24%2021,11.28%2021,13.75V21M7,21H3V9H7V21M5,3A2,2%200%200,1%207,5A2,2%200%200,1%205,7A2,2%200%200,1%203,5A2,2%200%200,1%205,3Z'%3e%3c/path%3e%3c/svg%3e)

%20-%20https://sketch.com%20--%3e%3ctitle%3eEmail%3c/title%3e%3cdesc%3eShare%20article%20via%20email%3c/desc%3e%3cg%20id='Article'%20stroke='none'%20stroke-width='1'%20fill='none'%20fill-rule='evenodd'%3e%3cg%20id='article-desktop'%20transform='translate(-291.000000,%20-905.000000)'%20fill='%233d4042'%20fill-rule='nonzero'%3e%3cg%20id='Group-3'%20transform='translate(280.000000,%20700.000000)'%3e%3cpath%20d='M12.5859376,205%20L25.5,216.098563%20L38.4140625,205%20L12.5859376,205%20Z%20M11,206.352162%20L11,221.582916%20L19.5446429,213.697123%20L11,206.352162%20Z%20M40,206.352162%20L31.4553572,213.697123%20L40,221.582916%20L40,206.352162%20L40,206.352162%20Z%20M21.1197917,215.049268%20L12.5212054,223%20L38.4787946,223%20L29.8802084,215.049268%20L26.1688988,218.240388%20C25.7827601,218.567837%2025.21724,218.567837%2024.8311012,218.240388%20L21.1197917,215.049268%20L21.1197917,215.049268%20Z'%20id='Shape'%3e%3c/path%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

'%20fill='%233d4042'%20fill-rule='nonzero'%3e%3cpath%20d='M317.048444,961%20C318.677807,961.001791%20319.998224,962.333083%20320,963.975866%20L320,963.975866%20L320,972.789759%20C320,973.478748%20319.446027,974.037283%20318.762667,974.037283%20L318.762667,974.037283%20L313.420222,974.037283%20L313.420222,980.619276%20C313.466211,981.335082%20312.928257,981.953082%20312.218333,982%20L312.218333,982%20L298.781667,982%20C298.071743,981.953082%20297.533789,981.335082%20297.579778,980.619276%20L297.579778,980.619276%20L297.579778,974.037283%20L292.237333,974.037283%20C291.553973,974.037283%20291,973.478748%20291,972.789759%20L291,972.789759%20L291,963.975866%20C291.001776,962.333083%20292.322193,961.001791%20293.951556,961%20L293.951556,961%20Z%20M311.486889,970.525371%20L299.513111,970.525371%20L299.513111,980.050743%20L311.486889,980.050743%20L311.486889,970.525371%20Z%20M314.395276,962.742345%20C313.970645,962.65481%20313.549254,962.905694%20313.420222,963.322865%20C313.394809,963.404999%20313.380715,963.490265%20313.378333,963.576269%20C313.380722,963.661209%20313.394821,963.7454%20313.420222,963.826423%20C313.529012,964.18316%20313.855609,964.426832%20314.225778,964.427444%20C314.659193,964.427644%20315.022348,964.096906%20315.066078,963.66215%20C315.109809,963.227395%20314.819907,962.829881%20314.395276,962.742345%20Z%20M317.130097,962.784571%20C316.813535,962.651298%20316.448506,962.723595%20316.20547,962.967701%20C315.962434,963.211807%20315.889338,963.579564%20316.020315,963.899239%20C316.151293,964.218915%20316.460504,964.427444%20316.803556,964.427444%20L316.803556,964.427444%20C317.274992,964.425655%20317.651006,964.045094%20317.651006,963.576269%20C317.652304,963.230394%20317.44666,962.917844%20317.130097,962.784571%20Z%20M311.783656,955%20C312.500482,955.040538%20313.043667,955.574507%20312.997231,956.192982%20L312.997231,956.192982%20L312.997231,959%20L297.002769,959%20L297.002769,956.192982%20C296.956333,955.574507%20297.499518,955.040538%20298.216344,955%20L298.216344,955%20Z'%20id='icon-print'%3e%3c/path%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

Tax News You Can Use | The Northern Trust Institute

Jane G. Ditelberg, Chief Tax Strategist

March 2, 2026

The Benefits Of Bunching: Charitable Planning After OBBBA

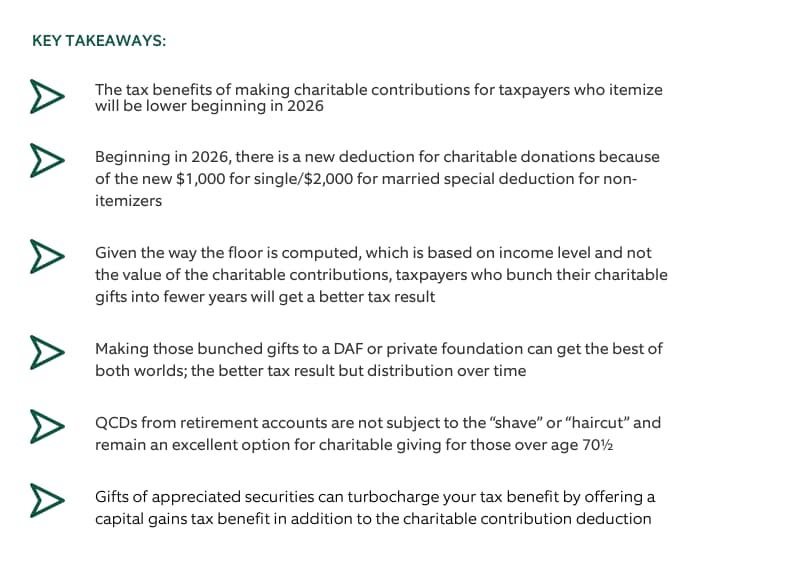

Among the provisions of the One Big Beautiful Bill Act (OBBBA) taking effect for 2026 and beyond are two provisions that, combined, can have a significant effect on the size of the income tax charitable deduction and the tax benefit from a taxpayer’s donation. Beginning this year, all taxpayers who itemize deductions will be able to deduct only that portion of their charitable contributions that exceeds 0.5% of their modified adjusted gross income (MAGI). Also beginning in 2026, those taxpayers in the 37% income tax bracket (single filers with taxable income over $640,600 or married taxpayers filing jointly with taxable income over $768,700) will have a portion of all itemized deductions disallowed.

What Is The “Shave” Or The “Floor?”

The provision that commentators have dubbed the “shave” or the “floor” is limited to charitable contributions by taxpayers who itemize. It denies a charitable contribution deduction for donations up to 0.5% of the taxpayer’s MAGI. For a taxpayer with $500,000 of MAGI, the first $2,500 in charitable contributions would not be deductible. This would mean paying an additional $875 (using the 35% bracket) in federal income tax this year that would not have been paid if the contribution had been made in 2025.

The floor applies to all taxpayers regardless of income level, although the amount of deductions shaved is based on each taxpayer’s MAGI. It is also not based on the amount of charitable contributions made in a year — the above-noted taxpayer with $500,000 of MAGI would have the same $2,500 exclusion whether their charitable contributions were $3,000 or $3 million.

The only exception to this floor is for cash contributions to public charities (other than donor advised funds (DAFs) and certain supporting organizations), which qualify for the deduction for non-itemizers: This deduction of up to $1,000 for single filers and $2,000 for married taxpayers filing jointly is available 2026 and beyond.

What Is The “Haircut” Or The “Ceiling?”

The OBBBA added another wrinkle for tax years beginning after January 1, 2026, for taxpayers whose income puts them in the 37% bracket. A portion of these taxpayers’ itemized deductions, including charitable donation deductions and other itemized deductions like state and local taxes and mortgage interest, is disallowed. The formula determining the amount of the disallowance is equal to 2/37 multiplied by the lesser of (a) the total amount of itemized deductions claimed for the year or (b) the amount of income being taxed at the highest marginal rate. It may be easier to understand this by looking at some examples:

Example 1:

Erika is a single taxpayer with $700,000 of MAGI and the following itemized deductions in 2026:

Due to Erika’s income, a portion of her itemized deductions will be disallowed. The 37% bracket starts at $640,600. Therefore, the disallowance is 2/37 multiplied by the lesser of (a) $59,400 which is the amount of Erika’s income taxed at the 37% marginal rate, or (b) $206,500, which is the net itemized deductions. Here, $59,400 is the lower number, so $3,211 of itemized deductions will be disallowed. This means that, due to the “shave and a haircut” rules, Erika will be entitled to deduct only $203,289 of the $265,000 spent on deductible items.

Example 2:

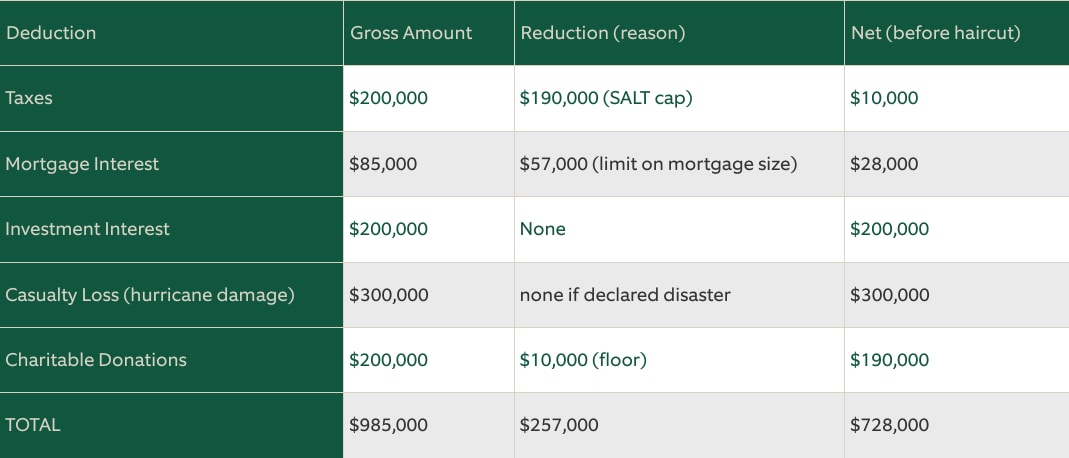

Brennan and Isabel are a married couple with $2 million of MAGI and the following deductions in 2026:

In this case, $1,231,300 of Brennan’s and Isabel’s income is taxed at the 37% rate and their net itemized deductions are $728,000: Therefore, the lower number of $728,000 is applicable. Of these deductions, $39,351 will be disallowed by the ceiling. This means that Brennan and Isabel will be able to deduct $688,649 of the $985,000 they spent on deductible items.

Example 3:

Katie is single and has MAGI of $400,000 in 2026. Her only itemized deduction is a charitable contribution of $50,000. While the haircut rule does not apply to Katie because she is not in the 37% tax bracket, the shave rule does apply. Katie is only allowed to deduct the amount of her charitable contribution that exceeds 0.5% of her MAGI. The floor for Katie is $2,000, so she may deduct only $48,000.

Example 4:

Jacob is single and has MAGI of $100,000 in 2026. He plans to take the standard deduction, but he has donated $5,000 to a public charity. He will be entitled to a charitable donation deduction of $1,000, which is not subject to the shave or haircut rules. This is a deduction he would not have been entitled to for the same gift made in 2025.

The Benefits Of Bunching

Given the structure of the floor limitation, taxpayers who itemize will often achieve a better tax result if they consolidate their giving into fewer years. The floor limit kicks in annually based on income, but it is not tied to the value of the charitable donations — the disallowance for the year is the same whether the gift is small or large. But annual gifts every year will each be subject to the floor. And if the taxpayer still wants to funnel the gifts to their chosen charities annually, they can pre-fund their planned charitable gifts for the next few years. Making a gift to a private foundation or DAF to be distributed over time can achieve both goals.

Example 5:

Grant and Lily each pledged to give $200,000 to their local hospital between 2026 and 2029. Each of them has annual income of $600,000, putting them in the 35% marginal rate backet. Grant plans to make four separate annual gifts of $50,000, and Lily plans to make a $200,000 gift in 2026 to satisfy her entire pledge. As the following table illustrates, Lily’s total deductions are $9,000 or 5% more than Grant’s over the four-year period.

Even if a taxpayer does not have a specific charitable donation plan in mind for the next four years, they can bunch their giving into a single year and blunt the impact of the floor by using a DAF or private foundation. If Lily gave her donation to a DAF in 2026, distributions to the hospital could be spread out over time in the same manner as Grant’s gifts are.

Is There A Way To Boost The Tax Benefit?

While the OBBBA has reduced the tax benefit of the charitable deduction generated by a donation, it has not changed the capital gains tax benefit available when a taxpayer donates appreciated securities instead of cash. The donation to the grantor is the same whether they give cash or securities, but gifting appreciated securities gives the grantor the added benefit of avoiding capital gains tax upon the sale of the securities. This increases the overall tax benefit to the donor. For example, if in the previous example Lily had made her gift using securities with a basis of $1 instead of using cash, she would avoid capital gains tax of nearly $40,000 on top of the income tax deduction for the gift to charity.

Are There Exceptions To The “Shave And A Haircut” Rules?

One type of charitable contribution not impacted by the floor or the ceiling is a qualified charitable distribution (QCD) from a traditional retirement account (including an inherited traditional retirement account) by a person over age 70 ½. A QCD provides a unique opportunity to make a charitable donation without taking the funds into income first. In a QCD, the retirement account owner directs the retirement account trustee to make a distribution (up to $111,000 per taxpayer for 2026) to a charitable organization. That amount goes directly to the charity. The taxpayer does not recognize any income and is not entitled to a charitable deduction, but it reduces the taxpayer’s AGI and income taxes by excluding the amount from income. Amounts used for a QCD count towards a taxpayer’s required minimum distribution (RMD) for the year, although the taxpayer can direct a QCD at age 70½, which is before the RMD requirement would start. Using the QCD for all or part of a taxpayer’s RMD can reduce their AGI, which can be helpful for Medicare premium purposes as well as qualifying for various deductions that are limited by AGI.

In addition, as noted above, the charitable deduction of up to $1,000 (single) or $2,000 (married filing jointly) allowed to those who take the standard deduction and do not itemize is not impacted by the floor rules.

%20scale(1,%20-1)%20rotate(-90.000000)%20translate(-22.445237,%20-21.357547)%20'%20points='21.2928054%2010.2071946%2022.707019%208.79298104%2030.8809213%2016.9668834%2015.4904479%2033.9221138%2014.0095521%2032.5778862%2028.119%2017.034'%3e%3c/polygon%3e%3c/g%3e%3c/svg%3e)