- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Global Economic Commentary | February 26, 2026

A Fight Without A Finish

U.S. trade policy is weighing on confidence but not activity.

If trade policy were like a boxing match, the U.S. had hoped tariffs would be a decisive, knockout blow. While many of America’s trading partners reeled, they stayed on their feet and are wearing down their opponent.

Last Friday, the U.S. Supreme Court moved to curtail the use of emergency economic powers to enforce tariffs. The ruling does little to change the broader trade posture as alternative legal pathways remain, but it underscores a deeper point: policy has become a source of uncertainty as much as leverage. Tariffs are looking more like a drawn‑out exchange in which all sides will be bruised.

Despite this, growth across major economies has proven more resilient than expected, carried by domestic demand and easier policy settings.

Following are our thoughts on how top markets are faring.

United States

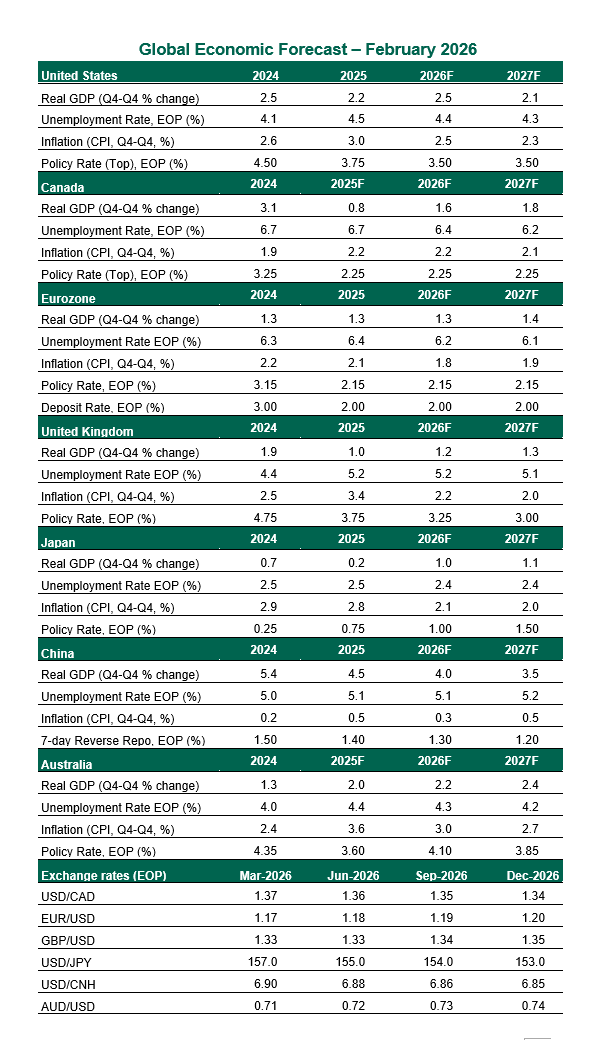

- After two quarters of outperformance, U.S. growth downshifted in the fourth quarter, with real gross domestic product (GDP) expanding at a 1.4% annualized pace. The slowdown was driven largely by a sharp pullback in government spending tied to the October–November shutdown. Consumer spending remained the economy’s main engine. The economy clocked a solid 2.2% expansion last year, demonstrating resilience which should remain on display this year. The Supreme Court tariff decision does not alter our growth outlook for the year ahead.

- At its January meeting, the Federal Open Market Committee left the federal funds rate and balance sheet policies unchanged. Two dissents in favor of a rate cut suggest additional easing is likely later this year, though there is little urgency. We expect one further rate reduction around midyear. The nomination of Kevin Warsh as Fed chair does little to alter that outlook. While Warsh has expressed firm views on the Fed’s role in financial markets, any move toward balance sheet reduction would likely be cautious and incremental.

Canada

- The Canadian economy lost momentum late in 2025 as tariffs, trade uncertainty, and slower population growth weighed on activity. The labor market reflects that cooling: employment fell at the start of the year. The Canadian unemployment rate dipped to 6.5%, largely owing to a shrinking labor force, pointing to persistent slack rather than renewed strength. Growth this year will be supported by sizable federal fiscal measures, but Canada’s outlook remains tightly linked to the upcoming US‑Mexico‑Canada Agreement (USCMA) review.

- The Bank of Canada appears comfortable that current interest rate settings are sufficiently restrictive to keep inflation anchored while the economy works through excess slack. We expect the central bank to stay on hold at the lower end of its neutral range over the forecast horizon. However, a renewed softening in growth or a more pronounced deterioration in labor market conditions would likely reopen the door to a modestly more accommodative stance.

Eurozone

- Growth performance across the eurozone was uneven in 2025. But activity is likely to converge gradually as 2026 unfolds. Germany is poised to stir from stagnation as fiscal policy turns more supportive, while France is likely to settle into a more modest but steadier expansion following the adoption of its long‑delayed 2026 budget. Southern Europe should continue to outperform, with Spain again leading the way. At the aggregate level, tight labor markets will underpin consumption, though recent softness in retail sales suggests households remain cautious. The industrial recovery is not yet in place, but signs point in that direction. The balance of risks remains skewed to the downside, given a tougher U.S. trade stance.

- With inflation broadly settled around the 2% target and activity steady, the European Central Bank is expected to remain on a prolonged hold. Absent a material deterioration in growth or a renewed inflation shock, the bar for policy action in either direction appears high.

United Kingdom

- U.K. activity disappointed in the second half of last year, with fading momentum setting up a weak handoff into 2026. While growth will improve a tad, it is unlikely to show a meaningful rebound over the course of the year. Business investment will be held back by weak profitability and fragile confidence. As the labor market loosens, wage growth is moderating. Fiscal policy is tightening. Political uncertainty will add to the headwinds, with leadership risk within the Labor Party rising. Taken together, the outlook points to another year of modest growth.

- Labor market indicators point to a gradual loosening rather than outright stress. The unemployment rate has edged higher, vacancies continue to drift lower, and wage growth has cooled to multi‑year lows. This backdrop supports our expectation of further, measured rate cuts from the Bank of England. Our base case remains two further cuts, bringing the policy rate down to 3.25% by the middle of the year.

Japan

- Japan closed out 2025 with muted momentum, growing at just a 0.2% annualized pace, with the weakness largely driven by volatile inventory swings. Underlying demand held up better, as both private consumption and business investment continued to expand modestly. Consumption should be firm this year as real incomes improve, supported by another expected solid round of spring wage negotiations and easing inflation. Exports have started the year strongly on a nominal basis, supported by demand related to artificial intelligence. However, shipments to China will be constrained by weak capital goods demand and rising geopolitical frictions.

- Japan’s policy mix is set to continue evolving gradually rather than decisively. The Bank of Japan is likely to stay on a slow normalization path, albeit with a higher estimate of the neutral rate than in past cycles. Fiscal policy, however, is set to move in the opposite direction. The administration has proposed a two‑year suspension of the consumption tax on food. While Prime Minister Takaichi has stressed commitment to responsible, proactive fiscal management, any drift toward more populist measures would complicate the fiscal arithmetic and raise the risk of renewed market turbulence.

China

- While China was able to meet its “around 5%” growth target last year, it is likely to settle for a slightly more modest 4.5%–5% objective for this year. China’s export run will remain an important contributor but will face greater scrutiny. Domestically, challenges abound. Fixed‑asset investment slipped into contraction for the first time since the early pandemic period last year, reflecting the persistent downturn in the property sector and constrained infrastructure spending. The real estate crisis has left important industries like steel, cement and materials with excess capacity. Local governments continue to prioritize debt reduction over new projects, failing to deliver a meaningful lift to new projects.

- Chinese policymakers are likely to maintain a proactive fiscal stance, with an emphasis on risk containment rather than aggressive stimulus. The People’s Bank of China will continue to rely on targeted easing, but at a measured pace. Taken together, these tools should help stabilize activity at the margin but are unlikely to generate a material growth impulse.

Australia

- Australia’s economy has gained traction, as both consumption and business investment pick up. Rising real disposable incomes have been lifted by last year’s rate cuts, tax relief, cost‑of‑living support, and solid wage growth. This has underpinned household spending. Investment has been lifted by a surge in data center construction and energy‑related infrastructure. Housing has responded forcefully to easier monetary conditions, with demand pulled forward and prices rising sharply. Overall, the backdrop points to building momentum and a more convincing growth profile as Australia moves into 2026.

- Renewed inflationary pressures, on the back of robust domestic demand, have forced a rethink at the Reserve Bank of Australia. The central bank reversed course with a 25-basis point hike earlier this month and is expected to follow up with another increase in the following quarter.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.