- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Asia Pacific Economic Outlook | April 10, 2026

Undertow

The APAC region faces outsized vulnerability to the economic fallout from the Middle East war.

In our last quarterly Asia‑Pacific outlook, we cautioned that regional economies were navigating shifting currents and that the waters ahead were far from calm. Few anticipated how quickly those currents would turn turbulent.

Asia‑Pacific economies are already feeling the effects of the Middle East war through higher energy costs, supply disruptions, and tighter financial conditions. For several economies, the shock has translated into acute fuel shortages, sharp price spikes, and rationing. Energy remains the primary transmission channel, but the fallout is broadening. Disruptions to critical inputs, including fertilizers and helium, raise the risk of spillovers into food production and industrial supply chains.

Governments have responded with a mix of emergency measures, demand restrictions, and market interventions. Central banks, for now, have trodden cautiously. Limited fiscal space along with currency pressures could force difficult policy choices should the conflict enter a renewed phase of escalation.

Energy market disruptions are likely to persist for months, even in a best-case scenario of a lasting ceasefire. The region will face a more challenging macro mix, with softer growth colliding with higher inflation risks.

Following are our views on how major APAC markets are poised to perform.

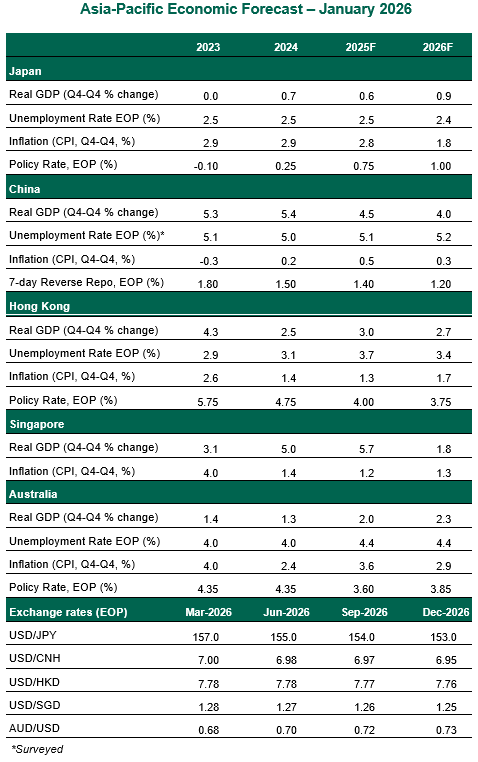

Japan

- Japan ended the year on a relatively positive footing, with real gross domestic product (GDP) registering a 0.3% quarter‑on‑quarter gain. However, the outlook has become more fragile since late February. Japan is particularly exposed to energy supply disruptions stemming from the conflict in the Middle East, given that over 90% of its oil imports and around 20% of its liquified natural gas (LNG) flows transit the Strait of Hormuz. Ample strategic reserves provide an important near‑term buffer. Sustained disruption or higher energy prices would still weigh on real incomes, despite robust nominal wage gains, and the broader growth outlook.

- Fiscal concerns may also resurface. The government has expanded fuel subsidies to cap gasoline prices, even as debate continues around a two-year suspension of the consumption tax on food. On the monetary side, the Bank of Japan (BoJ) has so far stood pat amid elevated market volatility and stagflation risks. We still expect the BoJ to deliver a rate hike this summer, with risks tilted toward one additional increase later in the year should inflation prove resilient and financial conditions remain orderly.

China

- China entered this challenging period in a position of relative strength. The country holds the world’s largest strategic petroleum reserves and maintains oil trade with both Russia and Iran. Export controls on fertilizers also help mitigate risks of agricultural shortfalls. These layers of preparation may help the economy come out relatively unscathed from shocks related to the war. Policymakers would likely tolerate a degree of imported inflation amid persistent domestic deflationary pressures, but higher energy prices alone are unlikely to deliver a sustained reflation with domestic demand still subdued. That said, China’s export sector is going to face a less supportive external backdrop, as higher global energy costs weigh on discretionary spending abroad.

- The National People’s Congress has set a real GDP growth target of 4.5%–5% this year, the lowest since 1991, reflecting a clearer acknowledgement of structural constraints. Policymakers are grappling simultaneously with a shrinking population and elevated debt‑service burdens across parts of the economy. Policy will remain geared toward stabilizing activity rather than engineering a meaningful growth acceleration, underscoring the shift toward prioritizing quality over quantity in China’s growth model.

Singapore

- Singapore has recorded unusually strong growth over the past two years. While the drag from tariffs on trade appears milder than initially feared, the conflict in the Middle East is set to slow momentum. Singapore’s heavy reliance on imported oil and gas leaves it exposed to energy market disruptions, which pose downside risks given Singapore’s role as a global refining hub. Growth is expected to slow this year.

- With energy costs set to push inflation higher, the Monetary Authority of Singapore is expected to tighten policy at its April meeting. However, given the largely supply‑driven nature of the shock and hopes for a durable ceasefire, we do not anticipate a prolonged tightening cycle.

Hong Kong

- Hong Kong’s economy has continued to gain traction. Last year’s equity market rally and the recovery in the property sector have strengthened wealth effects, supporting a rebound in consumption. Tax relief for households and SMEs announced in the recent budget will help sustain growth momentum. The conflict in the Middle East presents some upside risk to energy costs, but Hong Kong is relatively insulated given the lower weight of energy in the consumer price basket and access to alternative supply sources. Even so, financial spillovers remain a key secondary risk should hostilities be prolonged or re‑escalate.

- On the policy front, the Hong Kong Monetary Authority held its base rate at 4% following the Fed’s latest decision, citing heightened uncertainty linked to developments in the Middle East. With the Fed now expected to delay easing until later in the year, Hong Kong is likely to contend with higher‑for‑longer monetary conditions, adding a headwind to consumption and investment despite still‑supportive domestic fundamentals.

Australia

- Australia’s economy posted its fastest annual growth in nearly three years in the fourth quarter of 2025, establishing momentum heading into 2026. But the economy is now facing a supply shock alongside tighter domestic policy. Australia is particularly vulnerable to a global fuel shortage, with over 90% of its liquid fuel needs imported, largely routed through Asia and tied to Middle Eastern crude. The conflict is already weighing on business and household confidence and will amplify inflation pressures via higher energy, shipping, and transport costs. Recent monetary policy tightening will transmit through the housing market, reinforcing the slowdown.

- Rising inflation forced the Reserve Bank of Australia (RBA) to reverse course, delivering back-to-back rate hikes in February and March. While the risk of another hike remains, a ceasefire that evolves into a more durable easing of Middle East tensions would allow the RBA to shift to a prolonged hold. Pushing ahead with further tightening would add to downside risks to activity.

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.