US Economic Outlook | February 24, 2026

Thawing Out

A cold winter did not freeze the domestic economy.

The year got off to a cold start in the U.S., with many regions experiencing unusually freezing temperatures and precipitation. February has brought relief in both the weather and in economic reports.

Recent readings suggest the economy is making slow and steady progress. Inflation and employment did not reach feared extremes, but still leave room for improvement. Income tax refunds may support consumption in the near term, while the push for affordability policies may give households a more lasting tailwind. Policy uncertainty has not abated, but feels less disruptive.

Following are our thoughts on the U.S. economy.

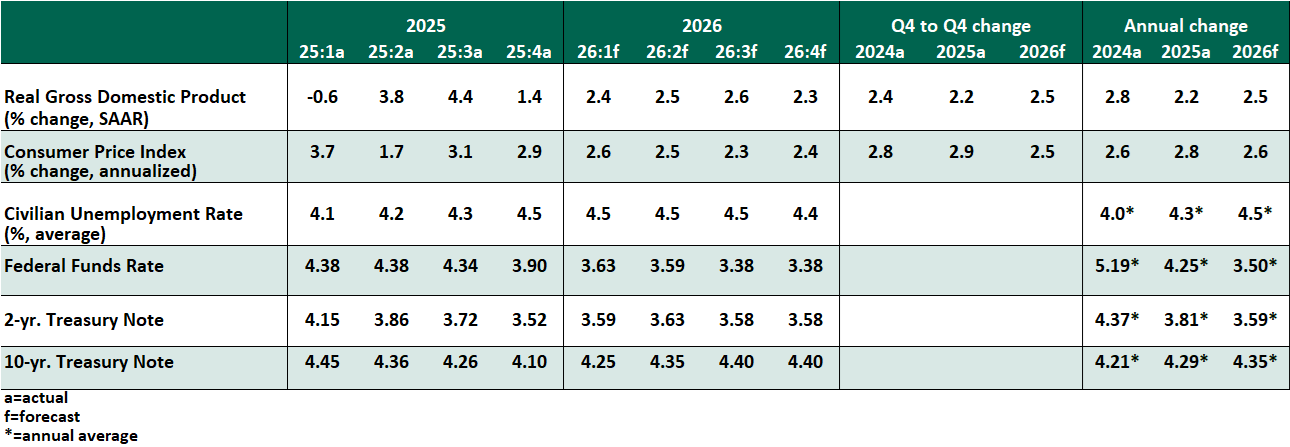

KEY ECONOMIC INDICATORS

INFLUENCES ON THE FORECAST

- After two quarters of outperformance, U.S. gross domestic product growth slowed to 1.4% at an annualized pace in the fourth quarter. A major decline in government spending due to the October-November shutdown was the biggest downward force. Consumer spending continued to lead growth. For the full year 2025, the economy grew 2.2% on an inflation-adjusted basis, demonstrating continued resiliency in the face of uncertainty.

- The January employment report exceeded expectations, with 130,000 jobs created. The unemployment rate ticked down one-tenth to 4.3%. Details of the report were mixed, with the majority of job creation confined to the healthcare sector. Annual benchmark revisions showed a cooler trend of payroll expansion had taken shape throughout 2025, reflecting cautious hiring and a stemmed flow of immigrants. While slower job creation is not ideal, it is encouraging that the economy has weathered a long-running slowdown without falling into recession.

- The consumer price index (CPI) for January reported a tame gain of 2.4% for the past year or 2.5% on a core basis (excluding food and energy). Through December, the price index on personal consumption expenditures held steady at 2.9%, or 3.0% core. Further downward progress may come slowly, and cost of living remains on consumers’ minds. However, wage gains are outpacing inflation, and the prospects of reflation are limited.

January is always a noisy month, as many firms make annual price changes at the start of the year. Tariff effects seemed likely to manifest, but import-dependent categories like apparel did not show outsized gains. Some tariff costs may still be passed through, but it appears that effects on final prices were far short of initial forecasts.

- Business sector productivity (real output per hour worked) posted a strong gain of 5.0% at an annualized rate in the third quarter, following 4.4% in the second quarter; a typical non-recessionary gain is less than 2%. A growing economy with slower hiring is leading to strong productivity. Artificial intelligence may be supporting gains in some sectors.

- At their January 28 meeting, the Federal Open Market Committee made no changes to the Fed Funds rate or their portfolio policies, continuing to add assets at a gradual pace to manage reserves. Two dissents in favor of a rate cut suggest that more easing is in store this year, but not with any urgency. We expect one additional rate reduction, at mid-year.

Fed Chair nominee Kevin Warsh is unlikely to alter the outlook for limited, cautious rate cuts. Warsh has expressed stronger views about the role of the Fed in financial markets, but any reduction to the balance sheet will be gradual.

- Major purchases are off to a slow start to 2026. Housing construction starts have posted four consecutive years of declines, while existing home sales in January fell by 8.4% from their level in December. Small inventories and winter weather are not supportive of housing turnover. Light vehicle sales also reached a three-year low in January. Policy measures may attempt to improve affordability, but consumer confidence will also need to pick up to see more activity.

- Markets have become an uneven barometer of geopolitical risk. The value of the dollar and the price of gold have been the most reactive indicators.

- The Supreme Court struck down the use of emergency economic powers to enforce tariffs. The U.S. trade posture will not change; many tariffs will return to force under other auspices, like national security. Refunds of past payments will require separate legal action.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.