Weekly Economic Commentary | December 19, 2025

Year-End Themes

What will we remember as we look back on 2025?

By Carl Tannenbaum, Ryan Boyle and Vaibhav Tandon

Editor’s Note: This week, we reflect on the themes that defined an eventful year.

Tariffs: Advance and Retreat

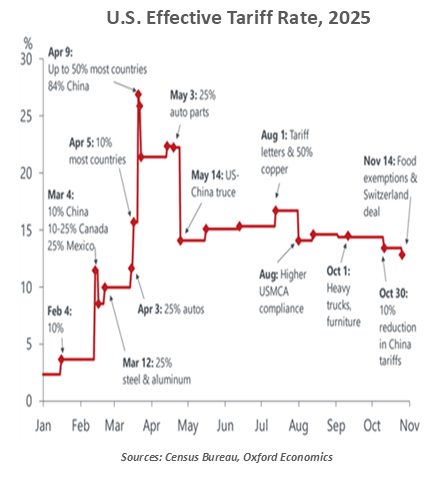

A look back at the economic stories of 2025 must begin with trade policy. President Trump zealously followed through on the central economic promise of his campaign. The size, speed and scope of tariffs exceeded all expectations.

In the first sixty days of this administration, levies related to fentanyl and migration were applied to Colombia, Canada, Mexico and China; steel and aluminum tariffs came back into force; and new protections were put in place for the auto sector. The main event came on April 2, “Liberation Day,” when the White House applied a 10% minimum import tax to all nations and placed arbitrarily higher tariffs on specific U.S. trading partners.

A bond market sell-off spurred the White House to temporarily defer reciprocal tariffs, an important signal that markets can provide feedback about policy. China tariffs were similarly scaled back when they proved damaging.

Tariff uncertainty peaked in the second quarter. Escalations have since been limited; a few significant nations like China, Japan and Korea have made progress toward truces and trade deals.

Business leaders struggled to make decisions this year, as they lacked clarity on their input costs. Investment and hiring turned sluggish. As 2025 draws to a close, however, fear of tariff escalation has largely dissipated. Actual tariff payments have not risen to the high headline levels, as many specific products have sustained exemptions.

The uncertainty has peaked but not passed. An imminent Supreme Court decision may overturn the reciprocal tariffs, bringing about a new set of levies with different justifications. Wherever tariffs ultimately land, they will be significantly higher than the old effective rate of 2.5%; businesses are still coming to terms with this cost.

They say that trees don’t grow to the sky. Neither do tariffs, but a new trade order is taking root.

The Fiscal Flip

For decades, fiscal fragility was a concern associated with developing and emerging markets. Currency crises, debt defaults, and multilateral bailouts became common in these domains. Advanced economies, by contrast, were beacons of stability: issuing debt in reserve currencies, enjoying deep capital markets, and benefitting from high levels of investor confidence.

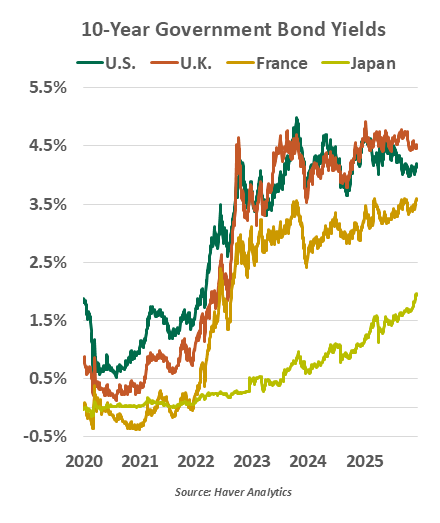

That script flipped in 2025. Fiscal policy dominated headlines as major economies wrestled with sustaining growth while managing debt in a world of higher interest rates. What used to be routine budget cycles turned into high-stakes exercises.

A summer reconciliation bill heavy on tax cuts and incentives unnerved the U.S. markets. America’s debt is estimated to climb as high as 200% of gross domestic product by 2054, up from 123% today.

Across the Atlantic, fiscal skepticism deepened. The U.K., still haunted by the gilt turmoil of 2022, pledged discipline. However, Britain’s back-loaded budget discipline risks renewed volatility. France, amid political turnover, has struggled to pass a compromise budget that balances deficit reduction with growth priorities. Japan, carrying the world’s highest debt ratio, doubled down on fiscal support to shield households from inflation.

Pandemic-era stimulus, followed by trade shocks and investments in national security, pushed advanced economies’ debt ratios to once-unimaginable levels. Rising interest rates compounded the strain, turning cheap debt into a costly burden. With frugality in short supply, investors demanded a premium for credibility once taken for granted, sending long-dated yields to multi-decade highs across several advanced economies. In some cases, investors started to reevaluate the safety of these debts, and rating agencies downgraded a series of sovereigns.

Although advanced economies still enjoy structural advantages, the year proved that confidence in them cannot be taken for granted. We don’t know where the tipping point is, just that we have gotten a lot closer to it.

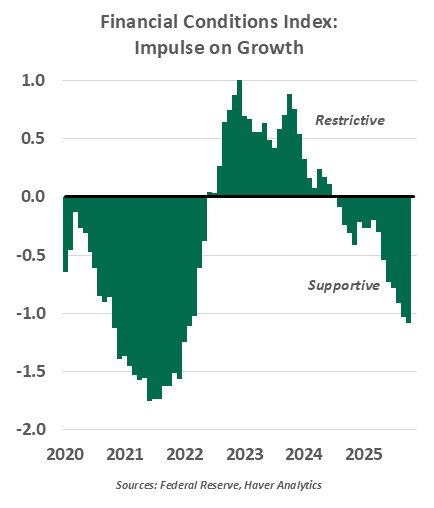

Walking the Monetary Tightrope

I recently watched a film about French high wire artist Philippe Petit’s death-defying walk between the Twin Towers in 1974. The image stayed with me, not just for its audacity, but because it mirrors a struggle unfolding today.

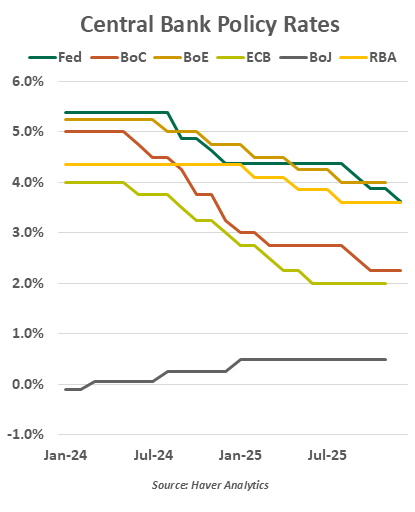

In 2025, central banks performed their own balancing act, suspended over a canyon of competing priorities. On one side lay the requirement of price stability: on the other, the need to safeguard economic activity and credibility.

For the Federal Reserve, the tensions were acute. Inflation has cooled from its peaks, but domestically-generated price pressures remained stubborn. The added risk of a trade war threatened to reignite cost increases, while housing dynamics kept inflation on consumers’ minds. The Fed’s 2% target collided with its employment mandate amid growing political pressure for faster easing. With its objectives in tension, policy debates intensified, and dissents to decisions multiplied.

From North America to Europe to Asia-Pacific, central banks faced similar conundrums. The Bank of Canada navigated the economic fallout from the U.S.-Canada trade war while guarding against retaliatory tariffs that could reignite inflation. The Bank of England wrestled with the combination of persistent wage and price increases and weakening activity. The slow retreat of British interest rates left households burdened by elevated mortgage costs.

In the eurozone, headline inflation eased, but high external uncertainty and resilient domestic activity kept the European Central Bank firmly data-dependent. The Reserve Bank of Australia’s cautious easing reflected a reversal in inflation trends late in the year.

The Bank of Japan’s (BoJ) priorities collided in reverse, as it sought to cautiously unwind decades of ultra-loose policy while preserving a fragile wage-price feedback loop. Policy in that country remained on hold for most of 2025 amid trade uncertainty and market volatility concerns.

The world’s central banks have been treading lightly on a high wire; one misstep could have sent inflation surging or tipped growth into contraction. The margin for error has rarely been thinner.

Return of the K

The pandemic created hardships across societies. But it had much more severe consequences for the lower echelons. Some essential workers had to continue working throughout, and were much more vulnerable to infection. Others in basic service sectors like leisure and hospitality endured extended job and income interruptions.

Government support hastened the economic recovery from COVID-19, but its impacts were uneven. Equity markets rallied quickly and powerfully, restoring lost wealth to the investor class. But it took unemployment two years to return to its pre-pandemic level. To describe this divergence of fortune, economists began referring to the recovery as “K-shaped.”

That term returned to prominence this year. Within the United States, wealth effects led spending by upper-income households to expand much more rapidly than it has for lower-income tiers. High-end retailers are prospering, while mid-tier chains are struggling.

There is also a K-shaped character to the performance of economies around the world. The United States is near the top of the pack among advanced economies with projected real growth of 2% this year. But many nations are looking at rates of less than half that. There were no winners in this year’s trade battles, but some countries lost more than others.

Economies perform best when disparities are modest. Major gaps serve as grounds for policies that are focused less on growth and more on allocation. Discontent among working classes is among the root causes of the trend toward deglobalization, which accelerated this year. Political partisanship also tends to increase when national income is unevenly distributed, making it difficult to reach consensus on a range of issues; this is among the ingredients in the fiscal stress we are seeing around the world.

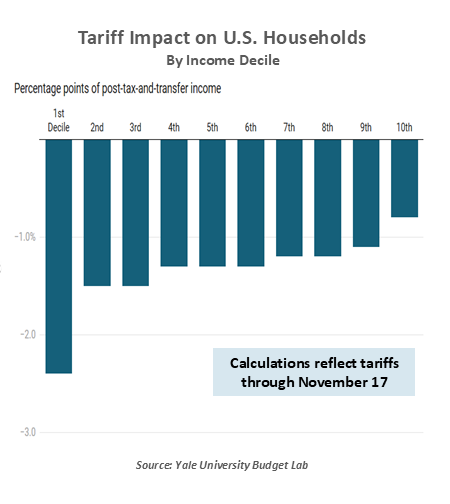

Ironically, some policies that ostensibly seek to help improve fortunes in the lower portions of the income distribution end up doing just the opposite. Analysis from the Yale University Budget Lab illustrates that the cost of U.S. tariffs will fall disproportionately on households with more modest means. Job gains in newly-protected sectors like manufacturing have yet to become visible.

Don’t expect much to change in the year ahead. The K is not going away.

Testing Our Limits

Every year, a new edition of the Guinness World Records book celebrates unlikely achievements. And every year, a subset of ambitious readers take it as a challenge to set a new record. 2025 saw new highs for holding one’s breath, building a human pyramid and running barefoot on Lego bricks.

If there were a financial section in the Guinness Book, it would have noted a number of new records this year. Equity markets are holding near all-time highs, and credit spreads in the bond market remain close to their all-time lows. Volatility has ticked up at a few intervals this year, most notably around April’s trade news; in each episode, it quickly settled.

The year’s great market performance is difficult to reconcile with an environment of high uncertainty. Trade policy has been disruptive, hiring is sluggish, and consumer sentiment is low. Investors worry that something has to give to bring the outlook into harmony with asset prices. Many observers fear this is the setup for a correction.

We are seeing outsized attention paid to any hints of bad news. A handful of large, idiosyncratic defaults raised the specter of “cockroaches” lurking in credit markets. Each quarterly earnings cycle brings intense scrutiny to the tech sector, with investors on edge to see if the growth cycle will carry on. Mere rumors about Fed leadership, tariff escalation, immigration, raw materials and renewed conflict have moved markets, but only briefly.

Most everyone would like to see asset prices march higher, and the faster the better. But a more measured pace, with periodic pauses to rebalance, may be more sustainable. Weathering occasional ups and downs may be uncomfortable, but it’s less painful than running on Legos.

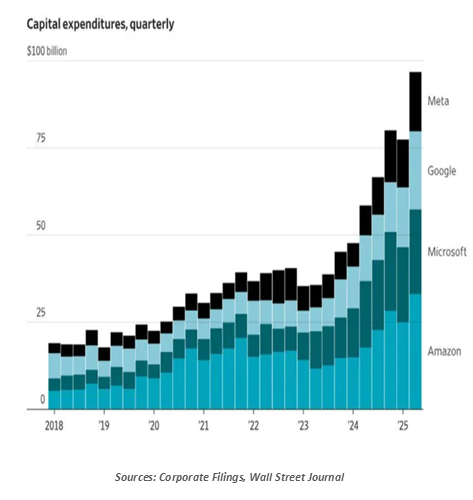

All In On AI

It’s hard to sound hip without using of contemporary jargon. In 2025, businesspeople striving to appear au courant sprinkled their sentences with terms like “agentic,” “slop,” and “hackathon.” Artificial intelligence (AI) has come to dominate our lexicon.

It has also come to dominate the global economy. Firms leading the AI charge have seen their share prices soar, creating wealth that has supported consumption. AI-related investments in software and facilities are booming. The combination of these elements has accounted for a substantial share of real growth this year.

The promise of AI-related productivity has given hope to those concerned about demographic decline and debt sustainability. But the path to realizing AI’s promise could be bumpy. Implementation will place immense pressure on the world’s power supply; nations unable to increase electricity generation will be at a disadvantage. AI systems require significant quantities of rare earth minerals, which are at the center of the trade war between the United States and China. Global regulators are paying attention to AI’s use of data and the potential misuses of the technology.

And AI appears to be affecting the employment prospects for recent college graduates, an early sign AI will both enhance and eliminate jobs. The labor market transition which may be in front of us could be challenging.

Any delay or retreat in the AI boom could be costly. Market valuations for tech leaders are very rich, and potentially vulnerable if the outlook changes. A correction would undermine household spending and capital investment. We don’t think we are witnessing a repeat of 1999, but we may be hallucinating.

Related Articles

Meet Our Team

Subscribe to Publications on Economic Trends & Insights

Gain insight into economic developments and our latest forecasts for the United States.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.